Disclosure: Some of the links you’ll encounter are unique links. Click and buy something and I’ll earn some money, at zero expense to you. Thank you!

This guide explains the key IRS rules governing Gold IRAs, including taxation, eligible investments, storage requirements, contributions, and withdrawals. Traditional Gold IRA distributions are taxed as ordinary income, while qualified Roth Gold IRA withdrawals are tax-free.

Only IRS-approved gold, silver, platinum, and palladium meeting strict purity standards may be held, and all assets must remain with an approved custodian in a secure depository. Home storage and prohibited transactions can trigger taxes, penalties, and loss of the IRA’s tax advantages.

You’ll also learn about annual contribution limits, Roth income restrictions, required minimum distributions (RMDs), early withdrawal penalties, and the tax benefits of holding precious metals inside an IRA instead of a taxable account. It highlights the differences between Traditional and Roth Gold IRAs, emphasizing that choosing the right account structure can significantly affect long-term tax savings and retirement planning.

IRS Rules for Gold IRA Investments: How Gold IRA Distributions Are Taxed (Overview)

Inside any IRA the nature of the underlying asset is irrelevant for tax purposes. The account wrapper controls the tax treatment, not the asset.

- Qualified distributions from a Roth Gold IRA are tax-free, regardless of how much gold has appreciated. The 28% collectibles rate never applies to gold held inside either type of IRA.

- Distributions from a Traditional Gold IRA are taxed as ordinary income at your marginal rate. Rates range from 10% to 37% depending on your total income in the withdrawal year.

In both types of gold IRA you can take distributions in cash, or you can take an in-kind distribution by receiving the actual physical gold coins or bars.

Both types of distributions are processed by the IRA custodian and reported to the IRS as retirement account distributions. Either way, the fair market value of the distribution on the date it occurs is what gets included in your taxable income for that year. The IRS values physical gold at its fair market value, which is generally based on the prevailing market price of the metal together with any applicable premium for the specific bullion product on the distribution date.

Early withdrawal before age 59½ triggers a 10% additional tax penalty on top of ordinary income tax for Traditional accounts. This additional tax is imposed under Internal Revenue Code Section 72(t), although certain IRS exceptions may eliminate the penalty in qualifying circumstances.

For Roth accounts, the 10% penalty applies only to the earnings portion of an early withdrawal Your original contributions can be withdrawn at any time without penalty because you already paid tax on them.

Whether Roth IRA earnings are taxable or subject to the penalty depends on whether the withdrawal qualifies as a qualified distribution, which generally requires satisfying both the five-year holding period and an IRS qualifying event, such as reaching age 59½.

Check this out next when you’re done reading my gold IRA taxation guide.

It’s a must-have info you must have, especially if you’re a proud American who’s curious about investing in gold, silver and other precious metals.

Eligible Metals and Products

A Gold IRA can only hold precious metals that meet IRS eligibility rules. The IRS permits four metals: gold, silver, platinum, and palladium, each with minimum purity requirements. Gold must be at least 99.5% pure, silver 99.9% pure, and platinum and palladium 99.95% pure.

In addition to purity standards, under Internal Revenue Code Section 408(m) only approved bullion coins and bars qualify for inclusion in a Gold IRA. Popular eligible products include American Gold Eagles, Canadian Maple Leaf coins, and Credit Suisse gold bars. Other commonly accepted IRA-approved products include American Silver Eagles, Canadian Silver Maple Leafs.

Collectible/numismatic coins and jewelry aren’t IRA-eligible even when they satisfy the required metal purity standards. The IRS distinguishes investment-grade bullion from collectibles because bullion value is primarily based on metal content, while numismatic value depends on rarity, historical significance, or collector demand.

Gold IRA assets must also be stored with an IRS-approved custodian and held in an approved depository rather than kept personally by the account owner.

IRA-Approved Storage Requirements

The IRS requires physical precious metals in an IRA to be stored with an approved custodian or trustee, such as a bank, credit union, or IRS-approved nonbank entity. This requirement applies to self-directed IRAs that hold alternative assets, including precious metals, and is intended to ensure compliance with IRS custody rules under Internal Revenue Code Section 408.

Gold home storage, personal safes, and private safe deposit boxes aren’t allowed and are treated as taxable distributions. The IRS considers it a transaction when an IRA owner takes personal possession of the metals. This results in ordinary income tax liability and additional penalties depending on the investor’s age and circumstances.

Early withdrawals trigger income taxes and a 10% penalty.

Approved gold IRA depositories offer segregated storage, where specific metals belong only to you, and commingled storage, where assets are pooled. Segregated storage costs more but provides clearer ownership records. Commingled storage is less expensive because the investor owns a specific quantity and type of metal rather than individually identified bars or coins.

All IRA-approved depositories use specialized security measures such as insured vault facilities, inventory tracking systems, and regular audits to verify stored assets.

Home storage IRA strategies exits, but they carry legal risks. These arrangements are often marketed as “checkbook control” or “home storage IRA” structures, but the IRS has challenged whether personally controlled precious metals satisfy IRA custody requirements.

Check this out next when you’re done reading my gold IRA taxation guide.

It’s a must-have info you must have, especially if you’re a proud American who’s curious about investing in gold, silver and other precious metals.

Prohibited Transactions

The IRS strictly enforces rules against prohibited transactions in self-directed IRAs. These restrictions are governed by Internal Revenue Code Section 4975, which defines disqualified persons and transactions that cause IRAs to lose their tax-advantaged status. The entire IRA loses its tax-advantaged status if a violation occurs causing the full account balance to be treated as a taxable distribution from the beginning of that year. For investors under age 59½ this distribution triggers an additional 10% early withdrawal penalty unless an exception applies.

Investors can’t use IRA-owned metals personally, use them as collateral, or engage in self-dealing transactions involving themselves, family members, or controlled entities. Disqualified persons include the IRA owner, spouse, certain family members, and entities controlled by those individuals.

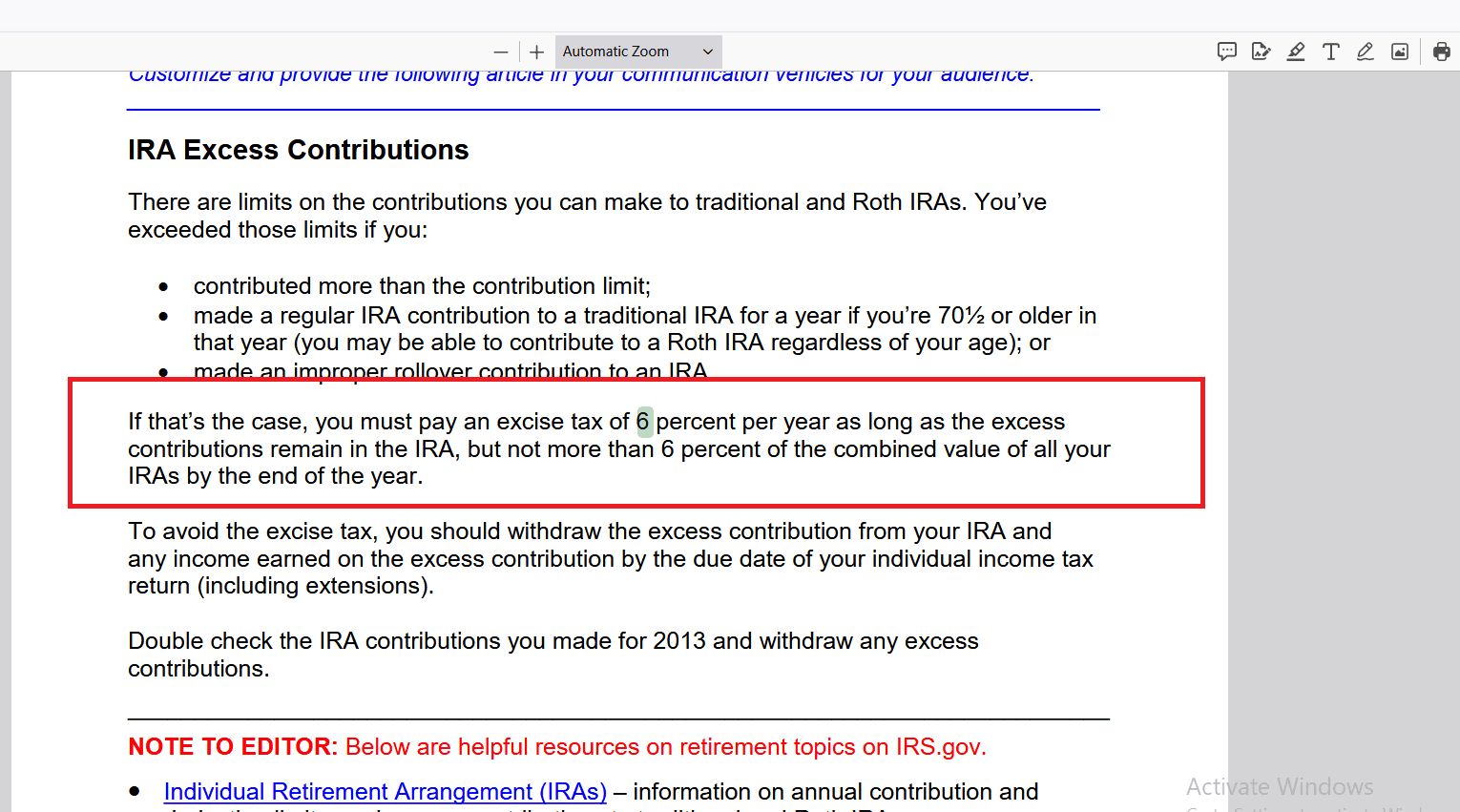

Purchasing collectible or non-qualifying coins that fail IRS purity requirements is another violation. Eligible precious metals must generally meet IRS fineness standards and be produced by approved mints or refiners, with exceptions for certain coins specifically allowed by law. Additionally, exceeding annual IRA contribution limits results in a 6% excise tax on excess contributions for every year they remain in the account.

Following IRS rules on storage, eligible metals, transactions, and contributions is essential to preserving a gold IRA’s tax benefits and avoiding severe penalties. Avoid compliance issues before they result in costly tax consequences by working with a qualified IRA custodian, tax professional, or retirement advisor.

Check this out next when you’re done reading my gold IRA taxation guide.

It’s a must-have info you must have, especially if you’re a proud American who’s curious about investing in gold, silver and other precious metals.

Contribution Limits and Deadlines

For this year the IRS limits total annual contributions to $7,000 per person across all IRA types (Traditional, Roth, and self-directed Gold IRAs). Individuals aged 50 or older can contribute up to $8,000 with the catch-up allowance. These limits are established under Internal Revenue Code provisions governing Individual Retirement Arrangements and are adjusted periodically for inflation by the IRS.

These limits apply collectively across all IRA accounts. For example, an investor can’t contribute the maximum amount to both a Roth IRA and a Gold IRA in the same year because the IRS applies one combined annual contribution limit across eligible IRA accounts.

Roth IRA contributions are restricted by income limits, though higher earners may use a backdoor Roth conversion strategy involving a Traditional IRA contribution and conversion. A backdoor Roth strategy typically involves making a nondeductible contribution to a Traditional IRA and then converting those funds into a Roth IRA, although tax consequences may apply depending on existing IRA balances.

This IRS rule requires conversions to be calculated proportionally across all Traditional, SEP, and SIMPLE IRA assets, preventing investors from selecting only after-tax dollars for conversion.

Traditional IRA contributions have no income limits, but tax deductibility can be reduced for individuals covered by workplace retirement plans. Employer-sponsored retirement plans such as 401(k) plans affect whether Traditional IRA contributions receive an upfront tax deduction.

Even nondeductible Traditional IRA contributions benefit from tax-deferred growth when used for gold investments. In a self-directed Gold IRA, these contributions are used to purchase IRS-approved precious metals while allowing investment gains to remain tax-deferred until distribution.

Check this out next when you’re done reading my gold IRA taxation guide.

It’s a must-have info you must have, especially if you’re a proud American who’s curious about investing in gold, silver and other precious metals.

Required Minimum Distributions (RMDs)

Traditional Gold IRA owners must begin taking required minimum distributions (RMDs) at age 73 under the SECURE 2.0 Act. This age requirement applies to individuals who reach age 73 after 2022, following changes introduced by the Setting Every Community Up for Retirement Enhancement (SECURE) 2.0 Act of 2022.

The RMD amount is based on the previous year-end account balance and IRS life expectancy tables. Most IRA owners use the IRS Uniform Lifetime Table to calculate their annual distribution amount, while different tables may apply to certain beneficiaries or individuals with significantly younger spouses. Missing an RMD result in a 25% penalty, reduced to 10% if corrected within two years. This excise tax is reported to the IRS and may be waived if the account owner can demonstrate that the missed distribution was due to a reasonable error and is being promptly corrected.

Gold IRAs require special planning because assets are held as physical metals. Owners can satisfy RMDs by selling gold for cash, taking an in-kind distribution of physical metals, or using another Traditional IRA to cover the required amount. When taking an in-kind distribution, the precious metals are transferred out of the IRA and become personally owned assets, with the fair market value generally treated as a taxable distribution.

Roth Gold IRAs do not require lifetime RMDs, allowing investors to keep gold invested and growing tax-free. This difference between Traditional and Roth IRAs is one of the main tax-planning considerations when choosing a retirement account structure for precious metals. However, inherited Roth IRAs follow separate distribution rules under current IRS regulations.

Early Withdrawal Penalties

Early withdrawals from a Traditional Gold IRA before age 59½ are subject to ordinary income tax and a 10% penalty, whether taken as cash or physical metals. The distribution is generally taxed based on the account owner’s ordinary income tax rate for the year in which the withdrawal occurs. Their fair market value at the time of distribution is used to determine the taxable amount if physical precious metals are distributed in-kind, The penalty may be waived for certain exceptions, including disability, qualified education expenses, first-time home purchases, certain medical costs, unemployment, SEPP withdrawals, birth or adoption, and federally declared disasters.

SEPP withdrawals, also known as substantially equal periodic payments under Internal Revenue Code Section 72(t), must follow specific IRS calculation methods to avoid triggering the early withdrawal penalty.

Roth Gold IRA contributions can always be withdrawn tax-free, while earnings are tax-free only after meeting both the five-year rule and age requirement. To be considered a qualified distribution, a Roth IRA withdrawal generally must satisfy the five-year holding period and occur after age 59½ or another qualifying event specified by the IRS. Investors may need to liquidate whole coins or bars to satisfy required distributions as physical precious metals can’t easily be divided like cash investments.

Check this out next when you’re done reading my gold IRA taxation guide.

It’s a must-have info you must have, especially if you’re a proud American who’s curious about investing in gold, silver and other precious metals.

Gold IRA Tax Rules: Traditional vs. Roth Structures

Choosing between a Traditional and Roth Gold IRA is your most important tax decision. Traditional accounts defer taxes until withdrawal, while Roth accounts require taxes upfront but allow tax-free qualified withdrawals. Both structures protect gold investments from the 28% collectibles capital gains tax that applies to precious metals held in taxable accounts.

Learn how Roth and Traditional IRAs compare in the table below.

| Feature | Roth Gold IRA | Traditional Gold IRA |

|---|---|---|

| Contribution tax treatment | After-tax (not deductible) | Pre-tax (may be deductible) |

| Growth inside account | Tax-free | Tax-deferred |

| Qualified withdrawals taxed? | No, tax-free | Yes, as ordinary income |

| Early withdrawal penalty (under 59½) | 10% on earnings only (contributions withdrawable penalty-free) | 10% plus ordinary income tax |

| Required minimum distributions | No RMDs during owner’s lifetime | Yes, starting at age 73 |

| Contribution limit | $7,000 ($8,000 if age 50+); subject to income limits | $7,000 ($8,000 if age 50+) |

| Income limits to contribute | Yes: phases out at higher MAGI levels | None (deductibility may phase out) |

| Collectibles rate (28%) applies? | No | No |

| Best suited for | Savers who expect higher tax rates in retirement | Savers who expect lower tax rates in retirement |

Capital Gains and IRS Classification

Gold you hold outside of your gold IRA is classified by the IRS as a collectible. This means gains on long-term holdings are taxed at a rate as high as 28% and this significantly cuts into your returns.

That same appreciation is not taxed as a collectible when you hold gold in a gold IRA.

Instead, in a traditional gold IRA gains are taxed as ordinary income when withdrawn. In a Roth gold IRA gains are tax-free if withdrawn under qualified conditions.

This classification change is one of the most overlooked tax benefits of having a gold IRA. It leads to a lower effective tax rate on your gold profits, especially when compared to selling personal holdings outside of a IRA.

References.

- IRA Excess Contributions- https://www.irs.gov/pub/irs-utl/OC-IRAexcesscontributions2014.pdf

Nikola Roza

Nikola Roza is the owner of Nikola Roza- Everything You Can Learn About Precious Metals. He writes for people who love precious metals and jewelry and who're interested in adding gold, silver platinum and palladium to their retirement portfolios. Nikola is passionate about gold IRAs and investing in multiple asset types for a safer financial future. He also runs a successful online jewelry store where you can buy precious metal jewelry and various replicas of famous coins and bars. Learn about Nikola here.