Disclosure: Some of the links you’ll encounter are affiliate links. If you click and buy something, I’ll get a commission. If you’re reading a review of some precious metals company, please understand that some of the links are affiliate links that help me pay my bills and write about what I love with no extra cost to you. Thank you!

Accelerated depreciation is a valuable tool for real estate investors and landlords seeking to maximize tax benefits and enhance cash flow. By understanding how it works, you can optimize your business investment strategy. This post provides a comprehensive overview of accelerated depreciation, including its benefits, calculation methods, and key considerations.

Table of Contents

Understanding depreciation expenses and tax deductions in real estate

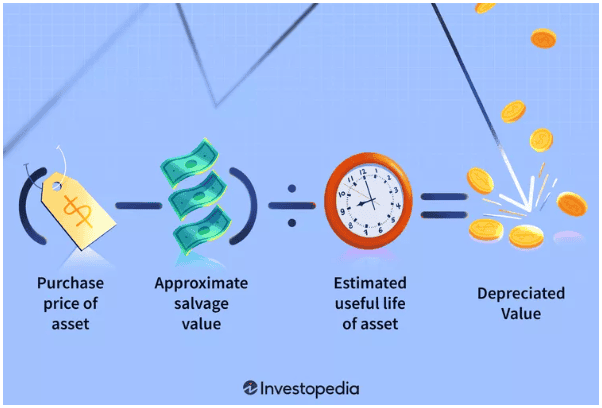

Depreciation is a concept in accounting that lets you deduct the cost of a tangible asset over its useful life. In real estate, this means deducting a portion of your property’s value each year to account for wear and tear.

By depreciating real estate assets, you reduce your taxable income and lower your tax bill. It’s like saying, “Hey, this office building is losing value as I use it to generate income, so I should get a tax break for that.”

Most assets depreciate over time until they reach their “salvage value,” the estimated value at the end of their useful life.

In the U.S., for example, residential rental properties are typically depreciated over a 27.5-year period under the Modified Accelerated Cost Recovery System (MACRS). This schedule ensures consistency in how property owners spread deductions across the asset’s useful life and helps prevent overstating annual expenses.

For a building, this is usually the cost of land plus whatever you could get for the old structure since the land itself doesn’t depreciate.

What is accelerated depreciation?

Accelerated depreciation is a type of depreciation method in which an asset loses its value faster in the early years of its useful life than in later years. This is in contrast to the traditional straight-line method (SLDM), where the asset depreciates at a constant rate over its entire life.

Imagine a new car. It loses a significant chunk of its value the moment you drive it off the dealership. Then, it depreciates more gradually over the following years. That’s similar to how accelerated depreciation works.

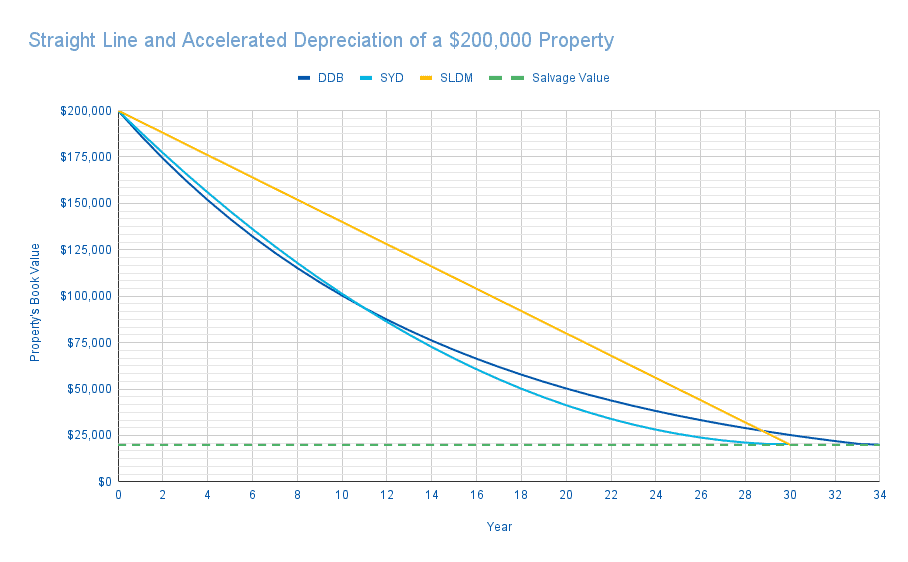

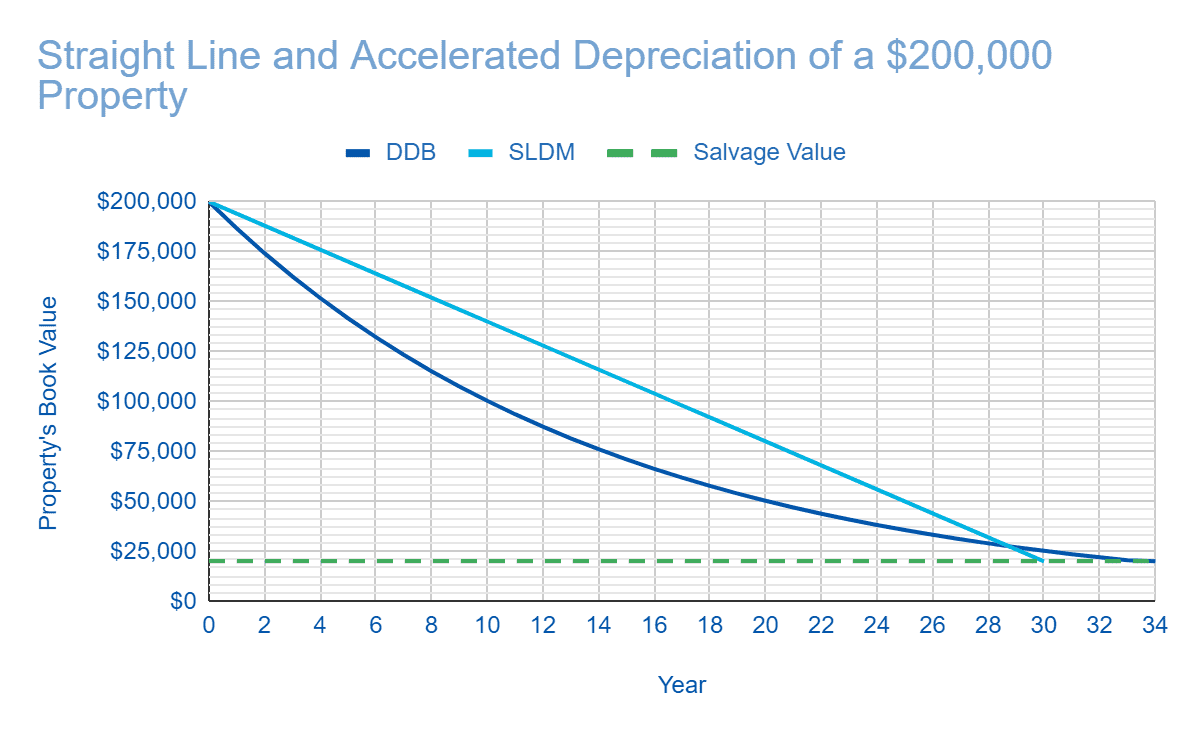

The logic is that we tend to utilize assets more when they’re new, making them depreciate faster at first than in later years. You can see this more clearly in the following graph showing different depreciation methods.

Notice how the property’s book value drops faster at first for the two blue lines (accelerated depreciation) than for the yellow straight line.

Making a case for accelerated depreciation in real estate

By deducting a larger amount sooner through accelerated depreciation, your taxable income can be reduced in the early periods, which can lead to significant tax savings and increased cash flow.

With these savings, you can:

- Cover expenses, especially when mortgage payments and other expenses are typically higher.

- Manage and improve your rental properties.

- Reinvest in your business.

- Allocate them towards other investments like data enrichment

Accelerated depreciation methods: A tool for real estate businesses

There are two main accelerated methods of depreciation:

- Sum-of-the-years’ digits (SYD)

- Double-declining balance (DDB)

Both work in different ways but offer similar benefits.

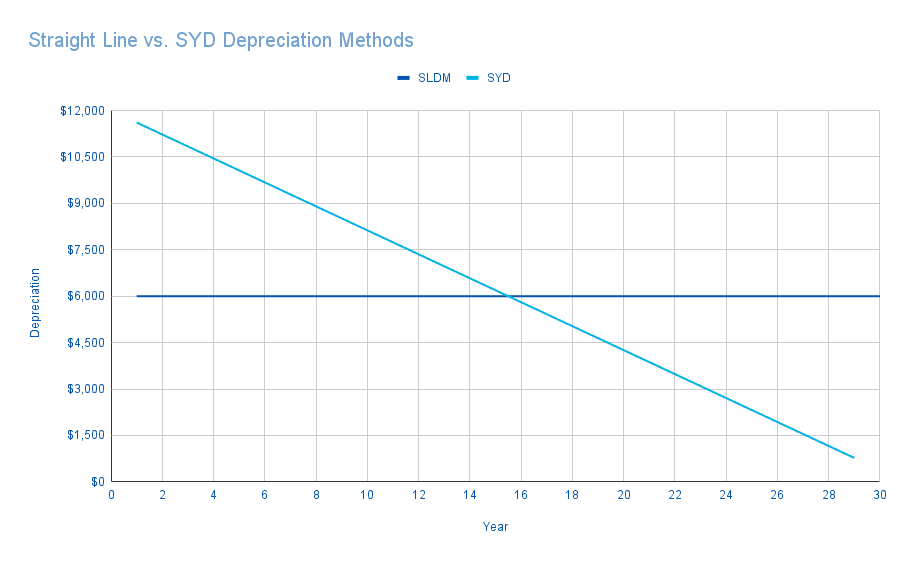

Sum-of-the-Years’ Digits Method (SYD)

The SYD method calculates the annual rate of depreciation based on a fraction that uses the remaining useful life as the numerator and the sum of the digits from year one to the asset’s useful life as the denominator (the sum of the years’ digits).

Sum-of-the-years’ digits accelerated depreciation formula

The formula to calculate each annual depreciation using the SYD method is:

Depreciation = (Depreciable basis) x (Remaining useful life / Sum of the years’ digits)

- The Depreciable basis is the cost basis minus the salvage value.

- The remaining life is the useful life minus the years in service.

- The sum of the years’ digits is the sum of all numbers from 1 to the useful life and is equal to n(n+1)/2, where n is the property’s total useful life.

Example

You invest in a residential property of 30 years. It cost $200,000, and you expect its salvage value to be $20,000.

- The basis for depreciation would be $200,000 – $20,000 = $180,000

- The Sum of the years’ digits would be 30(30+1)/2 = 465

During the first year (when the asset still has 30 years of useful life left), the depreciation would be:

- Depreciation = ($180,000) x (30/465) = $11,613

During the second year, the remaining life is now 29 years. In this case, the depreciation is:

- Depreciation = ($180,000) x (29/465) = $11,226

This method results in deductions that gradually decrease linearly over time, as you can see in the following graph.

Screenshot provided by the author

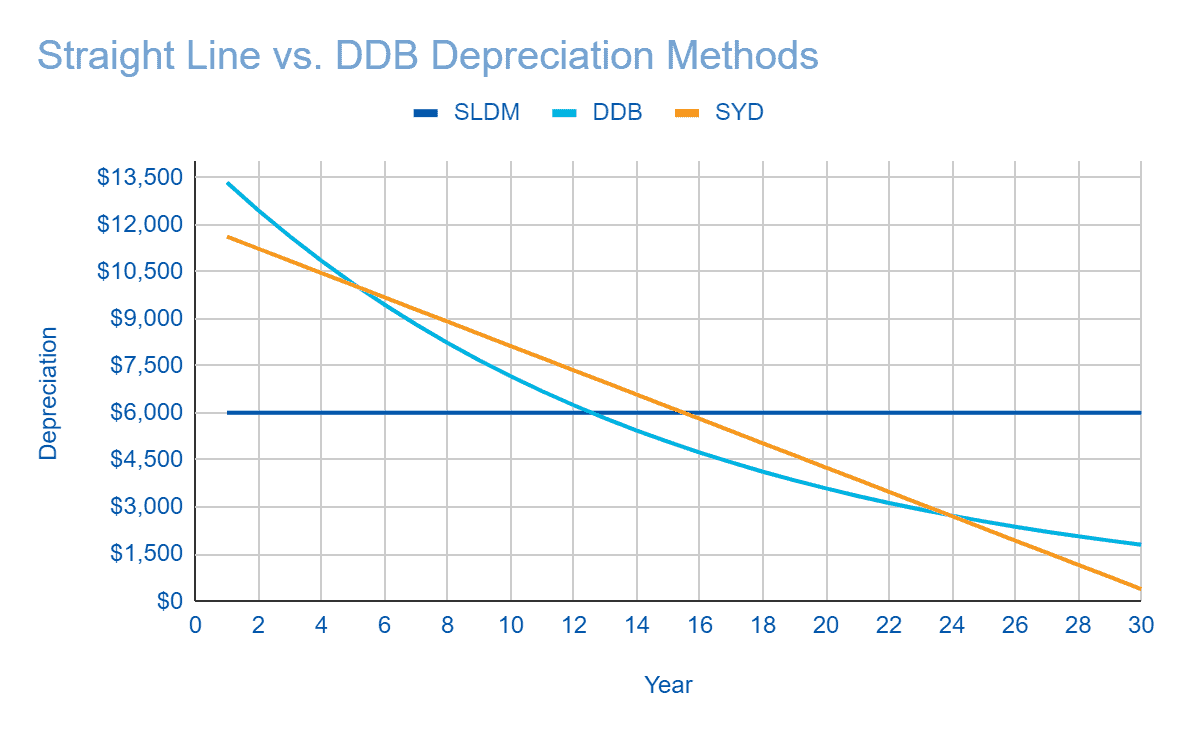

Double-declining balance method (DDB)

The DDB method depreciates assets at twice the straight-line depreciation rate. This results in the largest deductions in the first year, with the amount decreasing rapidly over time. The depreciation rate is fixed, but since the balance declines over time, so does the depreciation amount.

Double-declining balance formula

Depreciation in the DDB method is calculated with the following formula:

Depreciation = (Depreciable basis – Accumulated depreciation) x (2 / Useful life)

The Depreciable basis – Accumulated depreciation represents the asset’s current book value, which declines over time, giving the DDB method its name.

Example

Using the same example above, during the first year, the depreciation would be:

- Depreciation = ($200,000 – $0) x (2 / 30) = $13,333

During the second year, the accumulated depreciation is $13,333, so the new depreciation is:

- Depreciation = ($200,000 – $13,3333) x (2 / 30) = $12,444

And so on.

The DDB method provides a more aggressive depreciation schedule than the SYD method and offers the largest accelerated depreciation deductions upfront.

Screenshot provided by the author

A note on the DDB method

In the DDB method, the asset’s book value may reach the final salvage value before or after its useful life, depending on the particular initial conditions. Furthermore, the last depreciation is adjusted to ensure the final book value is the expected salvage value.

Screenshot provided by the author

Bonus depreciation

Bonus depreciation is a special depreciation allowance that allows you to deduct an extra portion of an asset’s initial cost in the first year it’s placed in service. Only some qualified properties are eligible for this tax break (personal properties don’t qualify).

You can combine bonus depreciation with other accelerated depreciation methods to further enhance tax benefits.

Bonus depreciation rules

Bonus depreciation is based on special rules from the IRS. For a qualified property acquired after September 27, 2017, and before January 1, 2023, the bonus depreciation percentage is 100%, allowing you to deduct the entire cost of the asset.

After that, the bonus depreciation rate declines by 20% each year to:

- 80% for real property acquired in 2023.

- 60% for tangible property acquired in 2024.

- 40% for real property acquired in 2025.

- 20% for property acquired in 2026.

Impact of accelerated depreciation on cash flow

Accelerated depreciation can significantly impact your cash flow, especially in the early years of property ownership. By front-loading annual deductions, you reduce your taxable income and, consequently, your tax liability. This translates to more cash on hand that can be reinvested back into your business.

Example

Let’s say your business has $100,000 in rental income, and you purchase a $200,000 property with a 20-year useful life. Here’s the impact on your income taxes in the first year, assuming a 21% Federal Corporate Income Tax rate:

| Method | Depreciation Expense | Taxable Income | Income Tax |

|---|---|---|---|

| Straight-line | $10,000 | $90,000 | $18,900 |

| DDB Method | $20,000 | $80,000 | $16,800 |

| Difference | $10,000 | -$10,000 | -$2,100 |

So, in this example, accelerated depreciation can increase your available cash by over $2,000.

Tax planning strategies with accelerated depreciation

Accelerated depreciation is also a valuable tool for tax planning. By understanding the applicable recovery periods and accelerated depreciation rules, you can optimize your deductions and minimize your tax liability.

For example, if you’re considering purchasing new office furniture for your rental business, knowing that it falls under the 7-year property category allows you to accurately calculate your depreciation deductions using the appropriate accelerated method.

Financial tools like credit cards can complement accelerated depreciation as a cash flow and tax planning strategy. Get a business credit card which provides flexible payment options and rewards. This helps property owners cover operational expenses, manage maintenance costs, and invest in property improvements.

Together, these tools provide greater liquidity and financial flexibility, allowing property owners to optimize both cash flow and tax benefits.

Unlock the Power of Accelerated Depreciation for Your Real Estate Business

Accelerated depreciation can help business owners enhance cash flow and plan their taxes better. By understanding the different methods, eligible properties, and calculation procedures, you can make informed decisions to optimize your real estate investments.

Remember, strategic tax planning is crucial for maximizing profitability and achieving your long-term financial goals.

P.S. Looking for more free resources? Head to Nikola Roza’s blog to explore more.

Author Bio: Israel Parada

Israel is a university chemistry professor, full-time writer, and part-time marketer passionate about data-driven SEO content writing and copyediting. He wrote about marketing, business, and personal finance for almost five years as the editor of Yore Oyster and is also a scriptwriter for the Two Bit da Vinci YouTube channel.

Headshot

Nikola Roza

Nikola Roza is a blogger behind Nikola Roza- SEO for the Poor and Determined. He writes for bloggers who don't have huge marketing budget but still want to succeed. Nikola is passionate about precious metals IRAs and how to invest in gold and silver for a safer financial future. Learn about Nikola here.