Disclosure: Some of the links you’ll encounter are unique links. Click and buy something and I’ll earn some money, at zero expense to you. Thank you!

A Guide to Choosing the Right Life Insurance Policy for Your Family’s Needs

Life insurance is an absolute must-have when securing your family’s financial future. It’s the safety net that can offer invaluable protection, making sure your loved ones are taken care of even in the worst-case scenario.

But with so many options, how do you choose the one that perfectly meets your family’s unique needs? And more importantly, how do you navigate this important decision without getting lost in the jargon and fine print?

Our goal is to arm you with the knowledge and tools you need to make an informed choice about life insurance for your family. We understand that every family is different — so what works for one may not necessarily work for another.

So it’s time to bring clarity to the complex world of life insurance and help you choose a policy that gives you peace of mind and secures your family’s future.

Step 1: Understand the basics of life insurance

Let’s start by getting your feet wet with the basics of life insurance.

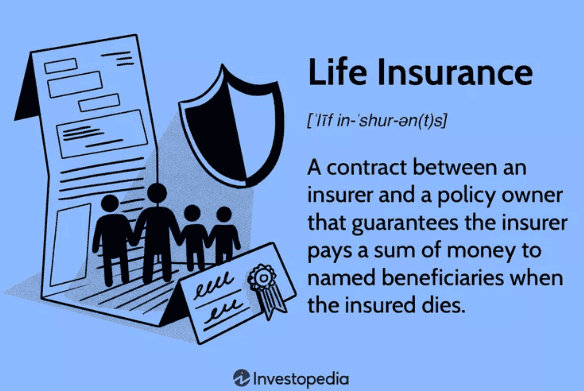

It’s a contract between you (the policyholder) and an insurance provider. You pay regular premiums, and in return, the insurance company promises to pay the people you’ve chosen as beneficiaries if you pass away.

These payments typically occur via:

- A lump sum

- An annuity

- Installment agreements

- Retained asset account

Purchasing a life insurance plan should give you comfort knowing that the people you care about most are well taken care of from a financial standpoint, even when you’re not there to provide it yourself.

A life insurance policy can cover anything from everyday expenses like groceries to larger expenses like college tuition for your children or even unforeseen veterinary expenses. Experiencing a flood or similar misfortune in your home can take a toll on your finances. Sometimes, hiring an exterior remodeling contractor can be pricey, and a good insurance plan after a flood could help you tackle this with ease.

The goal is to allow your family (including your beloved pets) to avoid further disruption after your passing by allowing them to live the same financial lifestyle and receive the same level of care.

Keep in mind that certain factors will impact your premiums, like:

- Age. Generally, the younger you are, the lower your premium will be.

- Gender. Statistically, women tend to live longer than men, which often leads to lower premiums for women.

- Health history. Insurers will review your medical history and may request an updated medical examination. Conditions like heart disease, diabetes, high blood pressure, or a history of cancer can increase your premiums.

- Lifestyle. Bad lifestyle habits like smoking, excessive drinking, or recreational drug use can increase premiums. So can high-risk activities like skydiving or racing cars.

- Occupation. You might face higher premiums if your job involves high-risk activities or environments.

Seeing “occupation” on that list might’ve raised an eyebrow. Well, here’s the scoop.

Say you work in the construction industry, where handling heavy machinery like a metal lathe is part of your daily grind (pun intended). The risk of potential accidents is, unfortunately, higher in such environments.

In serious workplace or road accidents, it’s often not just insurance that matters — medical documentation and legal support play a key role in claims and recovery. That’s where solutions like secure medical data platforms for personal injury cases help streamline the process, ensuring accurate records and collaboration between doctors and lawyers.

Now, picture this against a cubicle job in a leafy suburb, where the most significant danger might be the occasional paper cut or too much time spent sitting at your desk.

The contrast is pretty clear, isn’t it? When you encounter dangerous activity on the daily, there’s a higher likelihood that the insurance policy would need to kick in.

Step 2: Assess your family’s needs

Choosing the right policy starts with understanding your family’s unique financial situation. Consider your current income, expenses, and long-term goals — from paying off a mortgage to funding your children’s education.

Interestingly, recent research from 2024 shows that just over half of Americans currently have any form of life coverage, and many admit they still need additional protection. This highlights how easy it is to underestimate your family’s financial needs.

Ask yourself questions like, “How much would my family need to maintain their current lifestyle if I were no longer around?” or “Do I have any debts, like a home loan or student loans, that would need to be paid off?” The answers will help narrow in on your coverage needs.

And don’t forget to factor in those longer-term expenses, both predictable and unpredictable.

For instance, if you have young children, you may want to cover the future cost of their education or wedding. Or, if your spouse has underlying health concerns, you may need to cover the cost of assisted living or online doctor care in the future.

Remember, the goal here isn’t to get the cheapest policy or the one with the most benefits. It’s about finding a balance — a policy that gives your loved one the financial protection they need without breaking the bank.

After all, life insurance should be a safety net, not a financial burden.

Step 3: Determine the amount of coverage you need

Ok, let’s talk numbers. And if your eyes just glazed over, don’t worry. We’re keeping it simple.

As a general rule of thumb, your basic life insurance coverage should equal ten times your pre-tax annual income. For example, if you earn $60,000 per year, consider a policy with a minimum payout of $600,000.

For children, some insurance providers recommend an additional $100,000 per child, in addition to the 10 times the amount.

So, returning to the original example, if your annual salary is $60,000 and you have two children, your ideal coverage might start around $800,000.

- Base coverage: $60,000 (annual income) x 10 = $600,000

- Additional coverage for children: $100,000 x 2 = $200,000

- Total coverage: $600,000 + $200,000 = $800,000

Remember, it’s just a guideline and not a one-size-fits-all answer.

For instance, the “10 times income” rule doesn’t consider macroeconomic factors like inflation or your family’s future needs. The money your family might need in 10 or 20 years could be significantly more than they need now.

If you’re feeling overwhelmed, use an online life insurance calculator to get a quick estimate of how much coverage your family might need.

Step 4: Choose the right type of policy

Not all insurance policies are created equal. Just as engagement ring insurance policies may differ based on the ring’s value, type, and characteristics, life insurance policies vary based on your unique needs and scenarios.

Here are the basic types of life insurance available for your family:

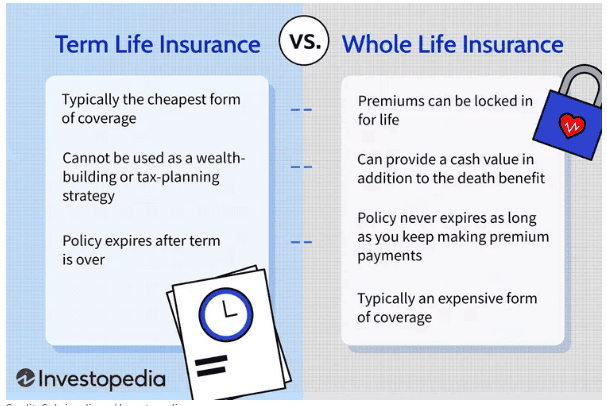

- Term life insurance. The most common form of life insurance. You choose a coverage amount and a term (usually between 10 and 30 years). If you pass away within that term, your beneficiaries will receive the payout. If you outlive the term, the policy simply expires.

- Whole life insurance. As the name suggests, this policy covers you for your whole life. A death benefit is guaranteed, and you can build cash value over time. Note that premiums are more expensive and considered part of a permanent life insurance policy.

- Universal life insurance. This policy is a little more flexible. It also includes a savings component that grows over time, allowing you to adjust your premium and death benefit as needed.

- Variable life insurance. This permanent coverage comes with an investment component. You can invest in your policy’s cash value, which means it can grow (or decrease in value) based on the performance of your investments.

Now, let’s look at a couple of examples.

Example 1: Term life insurance

Consider John, a 30-year-old new father of twins with a mortgage.

He wants to ensure his family has the necessary funds to maintain their lifestyle and pay off the house if anything happens to him before his kids are grown.

A 30-year term life insurance policy could be a cost-effective solution for John.

Example 2: Whole life insurance

Now, think about Lisa, a successful 40-year-old business owner with a ten-year-old daughter and seven-year-old son.

She has a sizable income and wants to leave a guaranteed inheritance for her children, as well as having the option of accumulating a cash value she can use during her lifetime.

A whole life insurance policy (or permanent policy) might be a great fit for Lisa.

Choosing the right policy is all about understanding your needs, assessing your financial situation, and confirming your risk tolerance.

Step 5: Evaluate and compare insurance providers

An insurance policy is only as good as the company that backs it. Therefore, the financial health and reputation of the insurance companies you’re considering are of the utmost importance.

It’s time to scrutinize the folks providing your life policies. You want an insurance provider with a solid track record and the financial strength to pay out claims decades later.

How do you assess a company’s financial health and reputation? Enter rating systems, like AM Best ratings. These independent agencies assess the financial strength and creditworthiness of insurance companies.

A high rating from AM Best (or a similar agency) can indicate a company is financially sound and well-equipped to pay out claims. These are the agencies you want to work with.

But don’t stop there. Once you’ve done the company search and created a shortlist of financially healthy, reputable companies, it’s time to compare custom quotes and policy details.

Remember, you’re not just looking for the cheapest policy. You’re hunting for the family life insurance coverage that offers the best value to meet your needs. So, peek under the hood at coverage amounts, term lengths, optional riders, and the potential for cash value to help you find the diamond in the rough.

Get peace of mind by investing in life insurance for your family

Securing your family’s financial stability is a reflection of your love, care, and foresight. Thoughtful financial planning ensures that your loved ones can continue to live comfortably, even in the face of unexpected challenges.

If you’re ready to take the next step toward building a safer, more secure future, explore more expert guides and practical resources on Nikola Roza’s blog. From money management to smart financial habits, you’ll find everything you need to make informed decisions that protect what matters most.

Nikola Roza

Nikola Roza is the owner of Nikola Roza- Everything You Can Learn About Precious Metals. He writes for people who love precious metals and jewelry and who're interested in adding gold, silver platinum and palladium to their retirement portfolios. Nikola is passionate about gold IRAs and investing in multiple asset types for a safer financial future. He also runs a successful online jewelry store where you can buy precious metal jewelry and various replicas of famous coins and bars. Learn about Nikola here.